Key Takeaways

- Understanding key tax rules is essential for landlords to reduce liabilities and boost long-term profitability.

- Major tax deductions like depreciation, insurance, and repairs can significantly lower your taxable income.

- Thorough record-keeping is crucial for maximizing deductions and protecting yourself in case of an IRS audit.

- Filing for a tax extension is a smart move if you need more time—accuracy matters more than speed when it comes to taxes.

You Need To Know These 4 Things About Taxes As A Landlord

Taxes are an unavoidable part of being a landlord.

However, understanding the nuances and intricacies of taxes can save you substantial money in the long run.

With that being said, let’s go over four things you need to know about taxes.

#1: Key Tax Deductions

Landlords can claim several different deductions, and these write-offs equal money in your pocket. Three of the major rental property tax write-offs are:

- Depreciation: This deduction helps you recover some costs associated with your property. You can deduct a part of the total cost of your property over time. Read more about depreciation in this article.

- Insurance: This write-off allows you to deduct premiums you pay for several kinds of insurance for your rental properties. Everything from landlord liability insurance to flood insurance is typically deductible up to some amount.

- Repairs: The cost of repairs is frequently deductible. This is good news because damages are an inevitable part of property ownership. Repairs like repainting your rental property, replacing cracked windows, and fixing gutters are great examples of deductible repairs.

#2: The Tax Cuts and Jobs Act (TCJA)

In 2017, Congress passed the Tax Cuts and Jobs Act, enacting some significant changes that impacted rental property owners. A lot of these changes were positive, too.

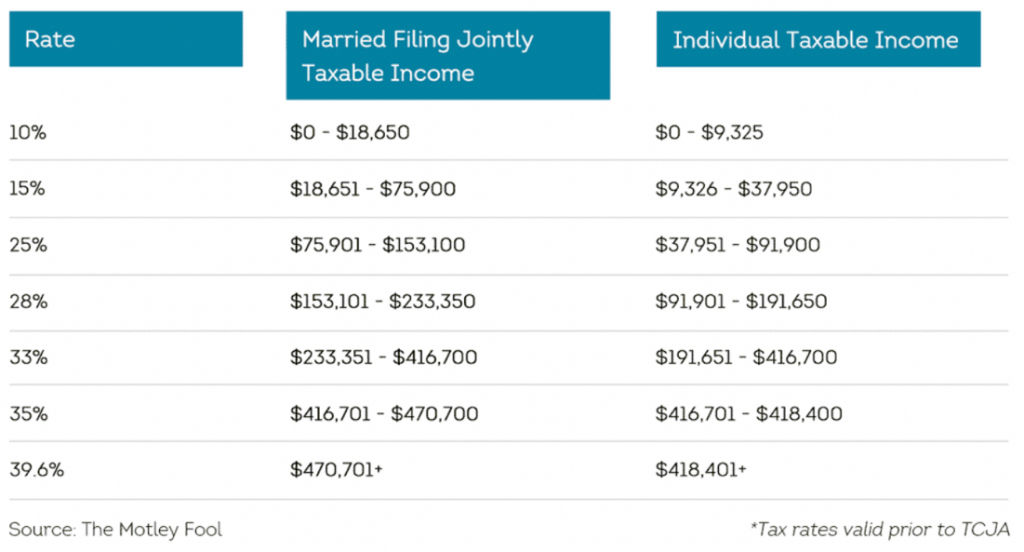

The first of these Tax Cuts and Jobs Act benefits is that individual tax rates are lower than they used to be. Here is a table of tax rates before the Act:

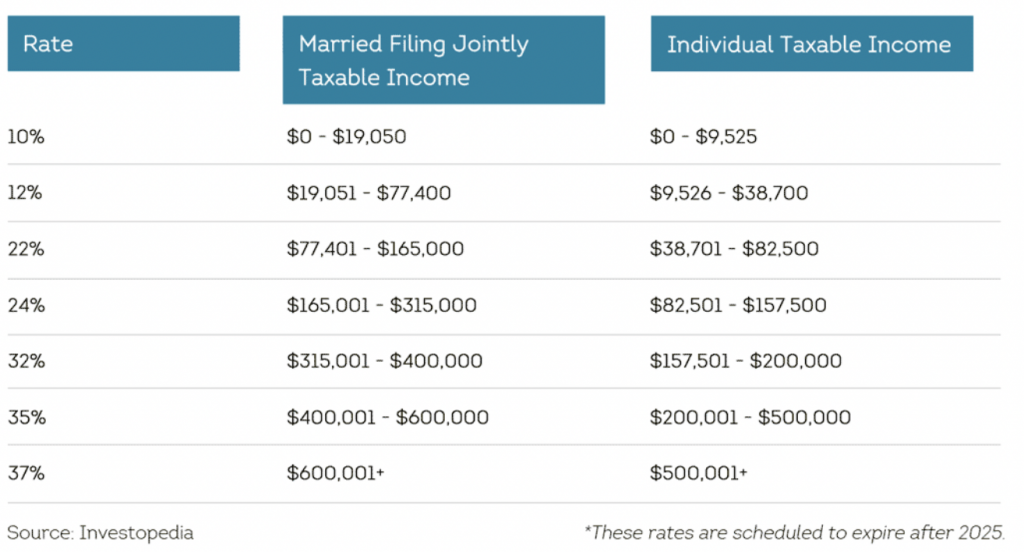

And here is a table of tax rates after the Act went into effect:

As you can see, you are likely paying lower income taxes due to the TCJA.

The second change worth mentioning is the qualified business income deduction (QBID, also known as the pass-through deduction). Before the enactment of the TCJA, if you had net taxable income from one of the listed pass-through businesses below, then that net income was taxed at your personal rates:

- Sole Proprietorship

- LLC treated as a Sole Proprietorship

- Partnership

- LLC treated as a Partnership

- S Corporation

Due to the TCJA, you may be able to put the QBID to use, depending on your total income level. If you can take advantage of this deduction, you’ll be able to deduct up to 20% of your net rental income.

The third significant change is that the section 179 expensing limit increased. Section 179 lets rental business owners deduct the cost of personal property used in their rental business, like appliances, certain equipment, or furniture.

The TCJA enlarged and increased the expensing limit from $500,000 to $1,000,000. This is applicable for property purchased and placed into rental service starting September 27, 2017, through December 31, 2022.

Before the enactment of the TCJA, landlords couldn’t deduct the cost of personal property used in residential rental units. From 2018 onward, this restriction is no longer a part of the law.

#3: Records You Need to Keep

If you only take one thing away from this article, keeping thorough records should be that thing. This is vital to taxes. Records can make or break your business in tax season. And you don’t want to get caught without pristine books if an audit from the IRS ever comes your way.

If you’re similar to most small landlords and haven’t formed a separate business entity to own property, you will need two main kinds of records for taxes: a record of your rental income and expenses and supporting documents for your income and expenses.

The records for your rental income and expenses help you determine whether your rental business earned a taxable profit or incurred a deductible loss for the year. And with these records, you’ll need to summarize your rental income and expenses for every rental property in your Schedule E form(s).

Receipts and supporting documents are critical (think credit card records and online payment records) because you need insurance in the event the IRS audits you. Certain expenses, like traveling expenses, need extremely thorough documentation. Maximizing your deductions and credits depends on your commitment to record-keeping. If you’re audited, the burden of proof is on you, so make sure you have the documentation to back up your claims.

Every deduction should at least have a paper trail detailing:

- What you bought for your rental activity

- The amount you paid

- Whom (or what organization) you purchased it from

For transportation, travel, entertainment, meals, gift deductions, and specific long-term assets you acquire for your rental business, you need to keep these kinds of records:

- Canceled checks

- Sales receipts

- Account statements

- Credit card sales slips

- Invoices

- Petty cash slips for small cash payments

One final tip for record-keeping: Make digital copies of everything. If something is a hard copy, it isn’t as secure as a digital copy. Keeping digital records will help you with organization and security. This is a critical component for any audit. You’ll thank yourself in the long run.

#4: Tax Extensions

Taking care of tax returns for all your properties can seem intimidating, especially if you’re a newer landlord. Even seasoned veterans can struggle when it comes to taxes and sifting through the plethora of information available regarding them.

So, to ensure you fill everything out correctly and accurately, don’t rush through the filing process. If you need more time, that isn’t a bad thing. You can apply for extensions that let you legally submit all necessary forms after the April 15 deadline.

There’s no shame in asking for an extension. Taxes are something you want to get right.

Conclusion

Obviously, there’s a lot more to landlord taxes than what we’ve covered. However, these four points provide a great starting point for all landlords. Don’t underestimate the power of doing the basics.

And, as always, if you need help or have questions, find a tax professional you trust. But, even with others’ help, it’s quite helpful to have your own knowledge base and ability to contribute to your tax forms.